2QFY2016 Result Update | Automobile

October 28, 2015

Maruti Suzuki

ACCUMULATE

CMP

`4,496

Performance Highlights

Target Price

`4,960

Y/E March (` cr)

2QFY16 2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

Investment Period

12 Months

Net Sales

13,934

12,315

13.1

13,425

3.8

Stock Info

EBITDA

2,269

1,532

48.1

2,189

3.7

Sector

Automobile

EBITDA Margin (%)

16.3

12.4

390 bp

16.3

-

Market Cap (`

cr)

135,802

Adj. PAT

1,226

863

42.1

1,193

2.7

Net Debt (` cr)

(12,652)

Source: Company, Angel Research

Beta

0.8

Results in line with estimates: Maruti Suzuki India Ltd (MSIL)’s 2QFY2016 results

52 Week High / Low

4,763/3,130

have come in in line with our estimates. Its revenues grew 13% yoy to `13,934cr,

Avg. Daily Volume

92,716

in line with our expectations of `14,007cr. Volumes grew 10% yoy while the

Face Value (`)

5

realization/vehicle grew 3% yoy on account of a better product mix. MSIL

BSE Sensex

27,040

maintained its record high margins similar to 1QFY2016; margins rose sharply

Nifty

8,171

by 390bp yoy to 16.3%, and are in line with our estimate. A favorable currency

Reuters Code

MRTI.BO

movement (depreciation of Japanese Yen and Euro vis-a-vis the Indian Rupee) led

Bloomberg Code

MSIL@IN

to lower imported raw material costs. This, coupled with decline in discounts,

boosted the operating margin. On the back of the robust operating performance,

the net profit came in at `1,226cr, in line with our estimate of `1,248cr.

Shareholding Pattern (%)

Promoters

56.2

Outlook and valuation: The passenger vehicle (PV) industry is well poised to post

MF / Banks / Indian Fls

18.9

double-digit growth over the next two years, given the improved consumer

FII / NRIs / OCBs

22.2

sentiments, better economic outlook, and softer fuel prices. Further, new launches

by MSIL, with it having recently introduced the premium hatch - Baleno and a new

Indian Public / Others

2.7

compact SUV, would enable it to gain market share, going ahead. Also, we

believe MSIL would be able to sustain higher margins (we have built in ~17%

Abs. (%)

3m 1yr

3yr

margin levels in our estimates for FY2016/17) given the subdued commodity

Sensex

(1.5)

0.6

45.2

prices and favorable currency rates. Reduction in discounts due to improved

Maruti Suzuki

7.1

42.7

228.9

industry outlook coupled with new product launches and benefits of operating

leverage would also enable MSIL to sustain margins at elevated levels. We view

MSIL as the best play on passenger vehicle demand recovery and expect 36%

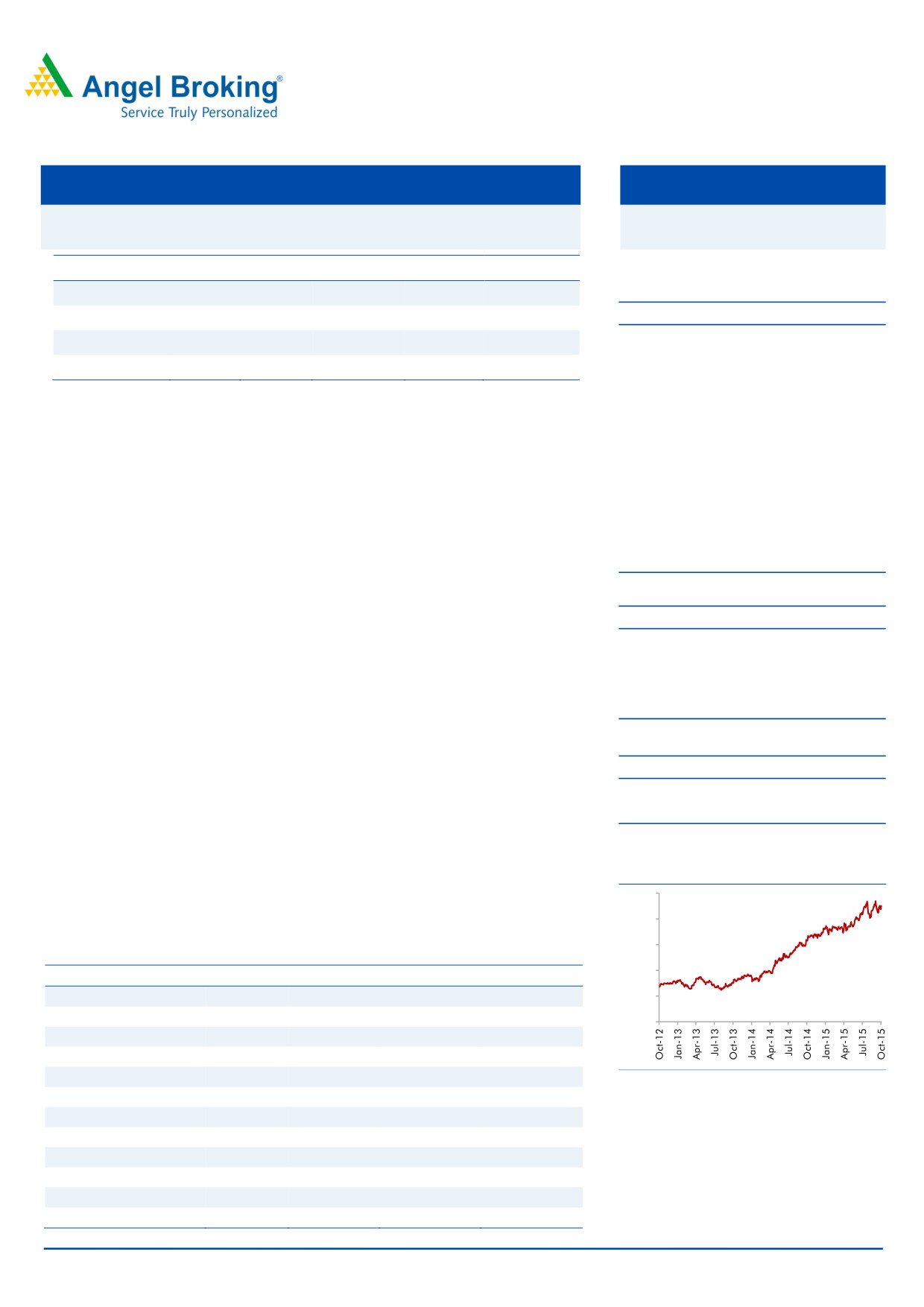

3-year price chart

earnings CAGR over FY2015-2017. We have retained our earnings estimates

5,000

given the inline results and maintain our Accumulate rating on the stock with a

4,000

price target of `4,960 (based on a PE multiple of 22x FY2017 EPS).

3,000

Key financials (post SPIL merger)

2,000

Y/E March (` cr)

FY2014

FY2015

FY2016E

FY2017E

Net Sales

43,701

49,971

57,865

68,104

1,000

% chg

1.4

14.3

15.8

17.7

0

Net Profit

2,783

3,711

5,324

6,810

% chg

21.0

33.4

43.5

27.9

EBITDA (%)

11.6

13.4

16.4

16.7

Source: Company, Angel Research

EPS (`)

92.1

122.9

176.3

225.5

P/E (x)

48.8

36.6

25.5

19.9

P/BV (x)

6.5

5.7

5.0

3.4

RoE (%)

13.3

15.7

19.4

21.2

RoCE (%)

16.2

20.5

26.3

28.4

Bharat Gianani

EV/Sales (x)

2.9

2.7

2.2

1.8

022-3935 7800 Ext: 6817

EV/EBITDA (x)

25.1

19.8

13.1

10.6

Source: Company, Angel Research

Please refer to important disclosures at the end of this report

1

Maruti Suzuki | 2QFY2016 Result Update

Exhibit 1: Quarterly financial performance

Y/E March (` cr)

2QFY16

2QFY15

% chg (yoy)

1QFY16

% chg (qoq)

1HFY16

1HFY15

% chg (yoy)

Net Sales

13,934

12,315

13.1

13,425

3.8

27,359

23,743

15.2

Raw-material cost

9,312

8,775

6.1

9,045

3.0

18,357

16,959

8.2

(% of Sales)

66.8

71.3

67.4

67.1

71.4

Staff cost

418

370

13.0

463

(9.7)

881

723

21.8

(% of Sales)

3.0

3.0

3.4

3.2

3.0

Other Expenses

1,934

1,638

18.0

1,728

11.9

3,662

3,142

16.5

(% of Sales)

13.9

13.3

12.9

13.4

13.2

Total Expenditure

11,664

10,783

8.2

11,236

3.8

22,900

20,824

10.0

Operating Profit

2,269

1,532

48.1

2,189

3.7

4,458

2,919

52.8

OPM (%)

16.3

12.4

16.3

16.3

12.3

Interest

18

35

(48.9)

19

(6.6)

37

73

(49.8)

Depreciation

669

599

11.8

672

(0.3)

1,341

1,182

13.4

Other Income

137

182

(24.6)

172

(20.3)

309

420

(26.4)

PBT (excl. Extr. Items)

1,719

1,080

59.1

1,671

2.9

3,390

2,083

62.7

Extr. Income/(Expense)

PBT (incl. Extr. Items)

1,719

1,080

59.1

1,671

2.9

3,390

2,083

62.7

(% of Sales)

12.3

8.8

12.4

12.4

8.8

Provision for Taxation

494

218

126.6

478

3.4

971

458

112.0

(% of PBT)

28.7

20.2

28.6

28.7

22.0

Reported PAT

1,226

863

42.1

1,193

2.7

2,418

1,625

48.8

Adj PAT

1,226

863

42.1

1,193

2.7

2,418

1,625

48.8

Adj. PATM

8.8

7.0

8.9

8.8

6.8

Equity capital (cr)

151.0

151.0

151.0

151.0

151.0

Reported EPS (`)

40.6

28.6

42.1

39.5

2.7

80

54

48.8

Source: Company, Angel Research

Exhibit 2: 2QFY2016 - Actual vs Angel estimates

Y/E March (` cr)

Actual

Estimates

Variation (%)

Net Sales

13,934

14,007

(0.5)

EBITDA

2,269

2,265

0.2

EBITDA margin (%)

16.3

16.2

10 bp

Adj. PAT

1,226

1,248

(1.8)

Source: Company, Angel Research

October 28, 2015

2

Maruti Suzuki | 2QFY2016 Result Update

Exhibit 3: Quarterly volume performance

Volume (units)

2QFY16 2QFY15

% chg (yoy) 1QFY15

% chg (qoq) 1HFY16 1HFY15

% chg (yoy)

A: Mini: M800, Alto, WagonR

110,987

98,992

12.1

104,801

5.9

215,788

201,721

7.0

A: Compact: Swift, Ritz, Celerio,Dzire

144,439

136,402

5.9

137,833

4.8

282,272

259,699

8.7

A: Mid-Size: Ciaz

10,546

1,658

536.1

13,374

(21.1)

23,920

2,177

998.8

Total Passenger cars

265,972

237,052

12.2

256,008

3.9

521,980

463,597

12.6

B: Utility Vehicles: Gypsy, Grand Vitara

21,083

17,102

23.3

15,550

35.6

36,633

32,369

13.2

C: Vans: Omni, Eeco

36,214

33,533

8.0

34,136

6.1

70,350

62,364

12.8

Total Domestic

323,269

287,687

12.4

305,694

5.7

628,963

558,330

12.7

Total Exports

30,066

34,211

(12.1)

35,635

(15.6)

65,701

63,462

3.5

Total Volume

353,335

321,898

9.8

341,329

3.5

694,664

621,792

11.7

Source: Company, Angel Research

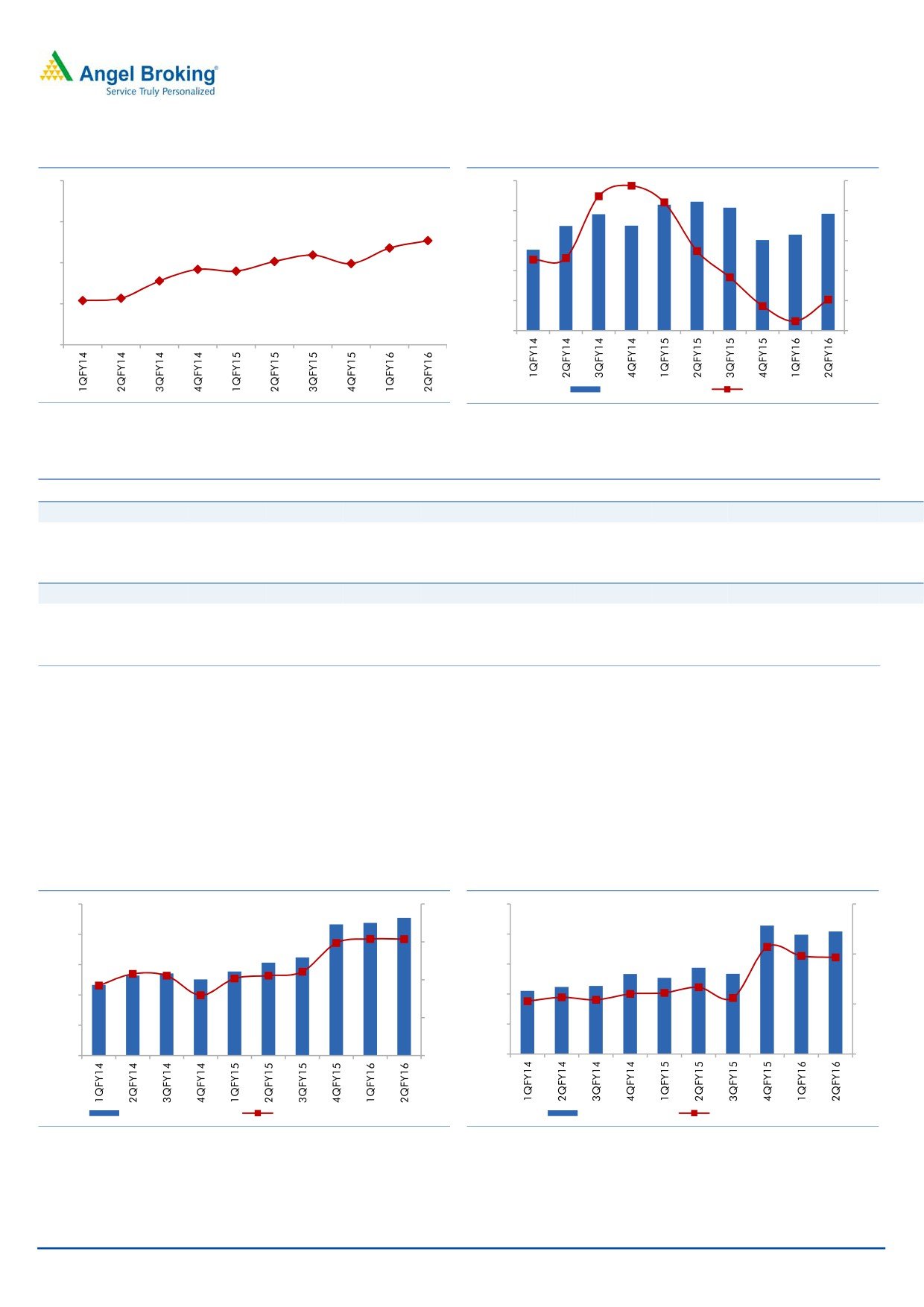

MSIL maintained its outperformance during the quarter, reporting a double-

digit volume growth. Improved consumer sentiments, better economic outlook,

and declining fuel prices boosted sales.

Realisation/vehicle grew 3% yoy owing to a better product mix with higher

volumes of Ciaz and Celerio. Further, the Contribution/vehicle improved

sharply by 19% due to currency benefits (weak Japanese Yen and Euro against

the INR), soft commodity prices, and a better product mix.

MSIL continued to outperform the domestic passenger vehicle industry,

registering a growth of 12% yoy in 1HFY2016 as compared to industry growth

of 6% yoy. Consequently, MSIL’s market share improved from 44.6% in

1HFY2015 to 47.3% in 1HFY2016.

Exhibit 4: Volumes grow in double-digits

Exhibit 5: Realisation & contribution per vehicle

400,000

25

390,000

140,000

350,000

20

380,000

300,000

15

120,000

370,000

250,000

10

200,000

5

360,000

100,000

150,000

0

350,000

100,000

(5)

80,000

340,000

50,000

(10)

0

(15)

330,000

60,000

Volumes (units)

growth yoy (%)

Realisation/vehicle (LHS)

Contribution/vehicle (RHS)

Source: Company, Angel Research

Source: Company, Angel Research

October 28, 2015

3

Maruti Suzuki | 2QFY2016 Result Update

Exhibit 6: Domestic PV market share trend

Exhibit 7: Discounting continues to soften

55

25,000

70

20,000

50

50

47.7

46.8

45.9

15,000

30

45.2

44.9

44.2

44.0

45

42.8

10,000

10

40.4

40.7

40

5,000

(10)

0

(30)

35

Discounting/vehicle

Growth (%)

Source: SIAM, Angel Research

Source: Company, Angel Research

Exhibit 8: Quarterly revenue and realization performance

2QFY2014 3QFY2014 4QFY2014 1QFY2015 2QFY2015 3QFY2015 4QFY2015 1QFY2016 2QFY2016

Domestic revenue (` cr)

8,693

9,691

10,696

9,831

10,595

11,039

12,070

11,694

12,447

Change yoy (%)

31.5

0.6

(7.2)

8.2

21.9

13.9

12.8

19.0

17.5

Domestic realization (`)

359,859

361,343

358,214

363,228

368,294

373,952

380,539

382,550

385,029

Change yoy (%)

14.3

0.8

(4.0)

(1.9)

2.3

3.5

6.2

5.3

4.5

Export revenue (` cr)

1,519

929

1,122

1,243

1,401

1,224

1,203

1,384

1,128

Change yoy (%)

84.3

(29.6)

(26.7)

37.0

(7.8)

31.8

7.2

11.3

(19.5)

Export realization (`)

446,450

465,291

427,038

424,943

409,517

426,347

407,217

388,382

375,175

Change yoy (%)

10.6

14.5

(2.8)

(1.2)

(8.3)

(8.4)

(4.6)

(8.6)

(8.4)

Source: Company, Angel Research

MSIL maintained record high operating margins of

16.3%, similar to

1QFY2016. Margins improved sharply by 390bp yoy. Currency benefits (JPY

and Euro depreciation against the INR) leading to lower raw material import

costs, coupled with lower discounts boosted margins.

The strong operating performance boosted profitability. The net profit grew by

a robust 42% yoy to `1,226cr, and the same is in line with our estimate.

Exhibit 9: Maintains record EBITDA margin

Exhibit 10: Strong operating performance boosts PAT

2,500

20

1,500

12

1,200

2,000

16

9

1,500

900

12

1,000

600

6

8

500

300

0

4

0

3

EBIDTA (`cr; LHS)

EBIDTA Margin (%; RHS)

PAT (`cr; LHS)

PAT Margin (%; RHS)

Source: Company, Angel Research

Source: Company, Angel Research

October 28, 2015

4

Maruti Suzuki | 2QFY2016 Result Update

Conference call - Key highlights

The share of petrol vehicles in the passenger vehicle industry continues to rise

given the narrowing differential between the price of petrol and diesel. The

share of petrol vehicles in the industry volumes rose to 54% in 2QFY2016 as

compared to 50% in 2QFY2015.

MSIL has been consistently outperforming the passenger vehicle industry on

back of new launches. In 1HFY2016, MSIL’s volumes grew 12% as compared

to the industry growth of 6%. Consequently, MSIL’s market share has risen

from 44.6% in 1HFY2015 to 47.3% in 1HFY2016. To further cement its

leadership position, MSIL recently introduced the premium hatchback

-

Baleno, which would be exclusively sold through “Nexa” showrooms.

MSIL continues to expand reach in rural areas. Despite weak sentiments in

rural areas on account of deficient rainfall and moderate growth in MSPs,

MSIL managed to report a 10% yoy growth in rural volumes in 2QFY2016.

The rural segment currently contributes by about one-third to the company’s

overall volumes.

MSIL is on track towards establishing its premium “Nexa” showroom network.

It currently has 80 Nexa showrooms and plans to increase them to 100 by the

end of FY2016. MSIL plans to further increase the Nexa count to 200 by

FY2017. Apart from the S-Cross, the recently introduced hatchback Baleno

would also be sold exclusively through the “Nexa” channel.

As per the company, certain export markets in Africa and Latin America are

facing a slowdown on account of slump in oil and commodity prices. Export

sales are likely to remain sluggish in the near term.

MSIL’s capacity utilization currently is at about 90% levels. As per the

company, the current production capacity of 1.5mn units is sufficient to meet

demand for FY2016; but the same would be enhanced to cater to the

anticipated increase in demand in FY2017. MSIL is in the process of

debottlenecking the existing plants in order to increase capacity as the new

Gujarat plant is expected to come on-stream only in FY2018.

MSIL has guided for a capex of `3,500cr for FY2016, to be incurred towards

new product introductions, enhancing the marketing infrastructure (particularly

Nexa showrooms), research and development, and maintenance.

MSIL indicated that the current dealer inventory stands at about 1 month,

which is the normal trend.

October 28, 2015

5

Maruti Suzuki | 2QFY2016 Result Update

Investment arguments

Per capita car penetration near inflexion point: In FY2012, passenger vehicle

penetration in India was estimated at around 16 vehicles/1,000 people

compared to around 70 vehicles/1,000 people in China. Moreover, India’s

PPP-based per capita is estimated to approach US$7,000 over the next four to

five years, which is expected to be the inflexion point for the country’s car

demand. Further, MSIL has a sizeable competitive advantage over new foreign

entrants due to its widespread distribution network (nearly 3,000 and 1,200

service and sales outlets, respectively), which is not easy to replicate.

Product launches in new segments to help outpace the PV industry: MSIL is

targeting to launch products in new segments in order to outgrow the

passenger vehicle industry. MSIL would introduce products in the compact

utility vehicle space which currently accounts for about 10% of the industry

volumes. Also, MSIL would introduce crossovers (vehicles combining features

of a car and a SUV) which would further enable it to gain market share.

Merger with SPIL to be a positive in the long run: MSIL has merged its

associate company, Suzuki Powertrain India (SPIL) with itself. SPIL

manufactures and supplies diesel engines and transmission components for

vehicles. SPIL currently supplies ~90% of its production to MSIL. We believe

the merger of SPIL with MSIL is a positive for MSIL given that MSIL itself is

setting up a new diesel engine facility (capacity of 300,000 units by FY2015)

in Gurgaon. Further, with increased product introductions in the diesel

segment (LCV and compact utility vehicle), the integration of SPIL will result in

better control over diesel engine sourcing, flexibility in production planning,

and managing fluctuations in market demand. Additionally, single

management control of diesel engine operations will result in better sourcing,

localization, and cost-reduction.

October 28, 2015

6

Maruti Suzuki | 2QFY2016 Result Update

Outlook and valuation

The passenger vehicle (PV) industry is well poised to post double-digit growth over

the next two years, given the improved consumer sentiments, better economic

outlook, and softer fuel prices. Further, new launches by MSIL, with it having

recently introduced the premium hatch - Baleno and a new compact SUV, would

enable it to gain market share, going ahead. Also, we believe MSIL would be able

to sustain higher margins (we have built in ~17% margin levels in our estimates

for FY2016/17) given the subdued commodity prices and favorable currency rates.

Reduction in discounts due to improved industry outlook coupled with new product

launches and benefits of operating leverage would also enable MSIL to sustain

margins at elevated levels. We view MSIL as the best play on passenger vehicle

demand recovery and expect 36% earnings CAGR over FY2015-2017. We have

retained our earnings estimates given the inline results and maintain our

Accumulate rating on the stock with a price target of `4,960 (based on a PE

multiple of 22x FY2017 EPS).

Exhibit 11: Volume assumptions

Y/E March

FY2011

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Mini: M800, Alto, WagonR

573,238

491,389

429,569

436,032

425,742

458,099

495,599

Compact: Swift, Ritz, Celerio, Dzire

369,754

345,886

424,873

450,393

514,638

571,248

651,223

Compact Utility Vehicle

12,000

36,000

Mid-Size: Ciaz

23,317

17,997

6,707

4,029

33,151

48,000

60,600

Executive: Kizashi

138

458

188

1

-

Total passenger cars

966,447

855,730

861,337

890,455

973,531

1,089,347

1,243,422

UV - Gypsy, Vitara, Ertiga, S-Cross

5,666

6,525

79,192

61,119

68,198

77,746

85,520

Vans - Omni, Versa, Eeco

160,626

144,061

110,517

102,115

128,973

141,870

156,057

Total passenger vehicles - domestic

1,132,739

1,006,316

1,051,046

1,053,689

1,170,702

1,308,963

1,485,000

Total passenger vehicles - exports

138,266

127,379

120,388

101,352

121,713

133,701

146,000

Light Commercial Vehicle

9,000

21,000

Total sales (domestic + exports)

1,271,005

1,133,695

1,171,434

1,155,041

1,292,415

1,451,664

1,652,000

% chg

24.8

(10.8)

3.3

(1.4)

11.9

12.3

13.8

Source: Company, Angel Research

Company background

Maruti Suzuki (MSIL), a subsidiary of Suzuki Motor Corporation (SMC), Japan

(which holds a 56% stake in MSIL), is the largest passenger car company in India,

accounting for ~50% of the domestic passenger car market. MSIL derives ~60%

of its overall sales from the small car segment and has a dominant position in the

segment with a market share of ~50%, led by popular models like Alto, Wagon R,

Celerio and Swift. The company operates from two facilities in India (Gurgaon and

Manesar) with an installed capacity of 1.5mn units. Also, MSIL has steadily

increased its presence internationally and exports now account for ~10% of its

overall sales volume.

October 28, 2015

7

Maruti Suzuki | 2QFY2016 Result Update

Profit and loss statement (post SPIL merger)

Y/E March (` cr)

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Total operating income

35,587

43,588

43,701

49,971

57,865

68,104

% chg

(2.8)

22.5

1.4

14.3

15.8

17.7

Total expenditure

33,074

39,358

38,611

43,268

48,381

56,698

Net raw material costs

28,108

32,559

31,314

35,008

38,764

45,571

Employee expenses

844

1,070

1,368

1,607

1,790

2,024

Other expenditure

4,122

5,730

5,928

6,654

7,826

9,103

EBITDA

2,513

4,230

5,090

6,703

9,484

11,406

% chg

(30.9)

68.3

44.8

31.5

41.5

20.3

(% of total op. income)

7.1

9.7

11.6

13.4

16.4

16.7

Depreciation & amortization

1,138

1,861

2,084

2,470

2,716

2,980

EBIT

1,375

2,368

3,834

5,074

7,497

9,449

% chg

(47.6)

72.3

27.7

32.3

47.7

26.0

(% of total op. income)

3.9

5.4

8.8

10.2

13.0

13.9

Interest and other charges

55

190

176

206

127

120

Other income

827

812

829

842

729

1023

Recurring PBT

2,146

2,991

3,659

4,868

7,370

9,329

% chg

(31.0)

39.4

27.7

33.1

51.4

26.6

Extraordinary income/ (exp.)

-

-

-

PBT

2,146

2,991

3,659

4868.2

7370.3

9329.4

Tax

511

599

876

1,157

2,046

2,519

(% of PBT)

23.8

20.0

23.9

23.8

27.8

27.0

PAT (reported)

1,635

2,392

2,783

3,711

5,324

6,810

ADJ. PAT

1,635

2,392

2,783

3,711

5,324

6,810

% chg

(28.6)

46.3

21.0

33.4

43.5

27.9

(% of total op. income)

4.6

5.5

6.4

7.4

9.2

10.0

Basic EPS (`)

54.1

79.2

92.1

122.9

176.3

225.5

Adj. EPS (`)

54.1

79.2

92.1

122.9

176.3

225.5

% chg

(28.6)

46.3

15.8

33.4

43.5

27.9

October 28, 2015

8

Maruti Suzuki | 2QFY2016 Result Update

Balance sheet statement (post SPIL merger)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

SOURCES OF FUNDS

Equity share capital

145

151

151

151

151

151

Reserves & surplus

15,043

18,428

20,827

23,553

27,280

32,047

Shareholders’ Funds

15,187

18,579

20,978

23,704

27,431

32,198

Total loans

1,078

1,389

1,685

180

200

200

Deferred tax liability

302

409

587

481

587

587

Other long term liabilities

97

104

239

105

105

105

Long term provisions

169

226

198

293

198

198

Total Liabilities

16,834

20,706

23,686

24,763

28,521

33,288

APPLICATION OF FUNDS

Gross block

14,735

19,801

22,702

26,462

29,962

33,712

Less: Acc. depreciation

7,214

10,002

11,911

14,202

16,918

19,898

Net Block

7,521

9,799

10,790

12,259

13,043

13,813

Capital work-in-progress

942

1,942

2,621

1,883

2,500

2,500

Investments

6,147

7,078

10,118

12,814

9,849

10,849

Long term loans and adv.

1,341

1,279

1,638

1,349

1,970

2,319

Other noncurrent assets

26

895

9

44

44

44

Current assets

6,325

5,695

5,359

5,202

8,998

12,775

Cash

2,436

775

630

18

3,472

6,354

Loans & advances

778

1,115

1,251

1,173

1,581

1,846

Other

3,111

3,805

3,478

4,010

3,945

4,575

Current liabilities

5,468

5,982

6,849

8,788

7,883

9,011

Net current assets

857

(287)

(1,491)

(3,586)

1,115

3,764

Total Assets

16,834

20,706

23,686

24,763

28,521

33,288

Note: Cash and bank balance includes term deposits with banks

October 28, 2015

9

Maruti Suzuki | 2QFY2016 Result Update

Cash flow statement (post SPIL merger)

Y/E March (` cr)

FY2012 FY2013 FY2014 FY2015 FY2016E FY2017E

Profit before tax

2,146

2,991

3,659

4,868

7,370

9,329

Depreciation

1,138

1,861

1,910

2,291

2,716

2,980

Change in working capital

227

512

2,112

1,440

(1,248)

233

Direct taxes paid

(251)

(533)

(876)

(1,157)

(2,046)

(2,519)

Others

(700)

(447)

(242)

154

(610)

(349)

Cash Flow from Operations

2,560

4,384

6,563

7,596

6,182

9,675

(Inc.)/Dec. in fixed assets

(2,963)

(3,810)

(3,580)

(3,021)

(4,117)

(3,750)

(Inc.)/Dec. in investments

(782)

(916)

(3,040)

(2,687)

2,966

(1,000)

Others

649

1,152

-

Cash Flow from Investing

(3,096)

(3,574)

(6,620)

(5,708)

(1,152)

(4,750)

Issue of equity

-

-

-

-

-

-

Inc./(Dec.) in loans

911

(514)

296

(1,505)

20

-

Dividend paid (Incl. Tax)

(217)

(217)

(696)

(884)

(1,597)

(2,043)

Others

(78)

(235)

312

(101)

-

-

Cash Flow from Financing

617

(966)

(88)

(2,388)

(1,577)

(2,043)

Inc./(Dec.) in cash

81

(156)

(145)

(501)

3,453

2,882

Opening Cash balances

96

281

775

630

18

3,472

Closing Cash balances

176

125

630

18

3,472

6,354

Note: Closing Cash balances excludes term deposits with banks and unclaimed dividend accounts

October 28, 2015

10

Maruti Suzuki | 2QFY2016 Result Update

Key ratios

Y/E March

FY2012

FY2013

FY2014

FY2015

FY2016E

FY2017E

Valuation Ratio (x)

P/E (on FDEPS)

83.1

56.5

48.8

36.6

25.5

19.9

P/CEPS

49.0

35.3

27.9

22.0

16.9

11.5

P/BV

8.9

7.0

6.5

5.7

5.0

3.4

Dividend yield (%)

0.2

0.2

0.3

0.6

1.2

1.5

EV/Sales

3.6

3.0

2.9

2.7

2.2

1.8

EV/EBITDA

48.4

37.3

25.1

19.8

13.1

10.6

EV / Total Assets

7.7

6.4

5.4

5.4

4.4

3.6

Per Share Data (`)

EPS (Basic)

54.1

79.6

92.1

122.9

176.3

225.5

EPS (fully diluted)

54.1

79.6

92.1

122.9

176.3

225.5

Cash EPS

91.8

127.5

161.1

204.6

266.2

324.1

DPS

7.5

8.4

12.0

25.0

52.9

67.6

Book Value

502.8

643.1

694.5

784.7

908.1

1065.9

Du-pont Analysis

EBIT margin

3.9

7.0

8.8

10.2

13.0

13.9

Tax retention ratio

76.2

0.8

0.8

0.8

0.7

0.7

Asset turnover (x)

2.7

2.2

1.9

2.0

2.3

2.5

ROIC (Post-tax)

7.9

12.2

12.7

15.6

21.6

25.6

Cost of Debt (Post Tax)

6.1

7.9

7.9

87.2

45.8

43.8

Leverage (x)

(0.5)

(0.3)

(0.4)

(0.5)

(0.5)

(0.5)

Operating ROE

7.0

10.7

10.6

53.8

33.2

35.2

Returns (%)

ROCE (Pre-tax)

8.8

14.7

16.2

20.5

26.3

28.4

Angel ROIC (Pre-tax)

18.3

15.2

16.6

20.5

29.9

35.1

ROE

11.3

12.4

13.3

15.7

19.4

21.2

Turnover ratios (x)

Asset Turnover (Gross Block)

2.7

2.2

1.9

1.9

1.9

2.0

Inventory / Sales (days)

16

16

14

19

13

12

Receivables (days)

9

12

12

8

11

11

Payables (days)

37

45

52

54

45

43

WC cycle (ex-cash) (days)

(12)

(18)

(26)

(27)

(21)

(20)

Solvency ratios (x)

Net debt to equity

(0.5)

(0.3)

(0.4)

(0.5)

(0.5)

(0.5)

Net debt to EBITDA

(3.0)

(1.8)

(1.8)

(1.9)

(1.4)

(1.5)

Interest Coverage (EBIT / Int.)

24.9

22.0

21.8

24.6

59.1

78.7

October 28, 2015

11

Maruti Suzuki | 2QFY2016 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange of India Limited. It is also registered as a Depository Participant with

CDSL and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is

a registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates including its relatives/analyst do not hold any financial interest/beneficial

ownership of more than 1% in the company covered by Analyst. Angel or its associates/analyst has not received any compensation /

managed or co-managed public offering of securities of the company covered by Analyst during the past twelve months. Angel/analyst

has not served as an officer, director or employee of company covered by Analyst and has not been engaged in market making activity

of the company covered by Analyst.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Pvt. Limited and its affiliates may

have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement

Maruti Suzuki

1. Analyst ownership of the stock

No

2. Angel and its Group companies ownership of the stock

No

3. Angel and its Group companies' Directors ownership of the stock

No

4. Broking relationship with company covered

No

Note: We have not considered any Exposure below ` 1 lakh for Angel, its Group companies and Directors

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

October 28, 2015

12